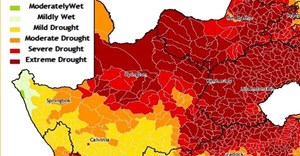

These provinces are heavily dependent on the agricultural industry and are the major producers of white maize in South Africa. KwaZulu-Natal, Mpumalanga, and Limpopo were also affected by the drought, bringing the total maize production down by about 30% from 2014 to 2015. Levels of South Africa’s national dams were at 54% in March 2016 compared to roughly 80% of capacity the previous year.

It is estimated that 1.25 million tons of white maize will need to be imported for the 2016/17 season, to supplement roughly 4.4 million tons of demand. Human consumption will account for 95% demand for imported and locally produced white maize. An additional 2.4 million tons of yellow maize will need to be imported to supplement roughly 6.04 million tons of demand. Animal and industrial consumption will account for 87% of demand for yellow maize. These imports could cause logistical issues despite South Africa having the needed infrastructure.

The weakening rand can be expected to have a negative impact on farmers who depend on imported animal feeds as well as end-consumers relying on agricultural imports, placing South African farmers as well as the general public in a difficult situation.

In addition to the increase in input costs, it is estimated that more than 180,000 livestock animals have been lost due to the drought. During January 2016, inflation was 6,2% while food and non-alcoholic beverage price indices indicated an increase of 6,9%. Early estimations indicate that the food basket could increase by up to 20% due to increasing agricultural input costs, expensive imports and slowed production caused by the drought.

It is expected that the current El Niño cycle ended during the first half of 2016. This could trigger the start of a La Niña cycle which might impact the agricultural production of the northern hemisphere. La Niña is the cooling of sea-surface temperatures in the equatorial Pacific Ocean which influences atmospheric circulation, and consequently rainfall and temperature in specific areas around the world. La Niña, Spanish for the girl, is the opposite of El Niño.

Many of the participants in the agricultural industry, including both crops and livestock farmers have over-indebted themselves in order to finance their operations through the recent difficulties. The government has started negotiations with selected banks to soften loan agreements in an attempt to aid farmers.

Despite the predicted end of El Niño, major challenges lay ahead this winter with limited feed available to support livestock. Favourable weather conditions will help in the recovery of the industry, but for the majority of farmers, the damage done in previous years will take many seasons to recuperate.

The agriculture industry is expected to face major challenges in the future with interrupted production caused by global climate change. Changes in the frequency of extreme weather patterns could have a significant effect on agricultural output, rising food prices and food security.

Increasing demand together with a strain on production will influence both developed and developing countries. While developed markets may see price fluctuations, developing countries could face food scarcity.

Developing African countries have large portions of their population employed in agriculture, with a significant part of this population dependent on plant-based staple foods. Increased demand will be driven by global population growth as well as the rapidly emerging middle class from growing economies. The rise in disposable income from middle-class households is expected to create a need for diversified diets. This trend leans especially towards animal proteins which will require a larger production of animal feeds in order to cultivate the needed livestock.

South African history has been shaped by agriculture. Although the country’s topographical composition and weather patterns are less than ideal. South Africa has restricted agricultural potential due to relatively high production costs. The annual average rainfall for South Africa, calculated over the past century, was slightly higher than 600 mm per annum. Large areas of the country are classified as semi-arid because of the low and irregular rainfall. Furthermore, only an estimated 12% of the country is suitable for agricultural purposes, leaving the sector vulnerable to changing weather patterns, as witnessed with the drought of the past two years.

Source: Department of Agriculture, Forestry, and Fisheries (Economic review of South African agriculture)

Despite this, South Africa is to a large extent self-sufficient in some of its major agricultural products. The country has a variety of produce owing to the diverse climate conditions throughout the country. This ranges from semi-dry grasslands in the central highlands, subtropical conditions on the East Coast and winter rainfall in the southern part of the Western Cape.

Some of the major South African produce includes maize, sugar, grapes, fish, tobacco, wool, wine and various fruits. Despite the availability of a wide range of produce, the ever-growing middle class has driven demand for specific imported agricultural products. In return South Africa has niche products to offer international markets such as rooibos tea and ostrich meat which appeals to increasingly health-conscious buyers. Seasonal production runs countercyclical to countries in the northern hemisphere, allowing South Africa to capitalise on exports to markets in the US as well as Europe.

Deregulation in the agriculture industry posed some challenges for local farmers regarding competitiveness with international markets. The growth in local poultry demand is being increasingly met by imported products, resulting in slowing growth in the poultry industry over the past five years.

However, income from poultry in 2015 amounted to R37.155 billion, second only to the revenue produced by red meat. The current drought is posing an additional threat to these industries impacting agricultural feeds, a major input cost. Lower local crop production has created a need for imported animal feeds, creating obstacles when coupled with the current rand depreciation.

Agriculture’s contribution to the South African GDP has shown a steady decline in the last half-century. The decrease is largely attributed to other industries growing at a higher rate. Agriculture only contributed 1,9% to the total GDP in 2015 compared to 6% in the 1970s. With this decreasing contribution to total GDP, agriculture still accounts for roughly 6% of total employment in South Africa.

This seemingly small industry has a significant impact on South Africa. Employment and high food prices affect a large portion of the population. It is not only a major source of income for numerous households in rural areas but also serves as a source of food.

Source: Statistics South Africa (Agricultural Survey 2014)

Issued by Coface, international credit insurer